This is my talk from 2012 Startup School, pretty much exactly as delivered.

It's been more than 7 years since we started YC. In that time, we've funded 467 startups so I've seen a lot of patterns. There's a talk I always want to give at the beginning of each batch, warning everyone about things that I know are probably going to happen to them. I finally wrote down all my thoughts and I'm going to share them with you now.

We all know that a lot of smart and talented people start startups. You see huge numbers of startups getting started, and yet there are actually only a handful of startups that are big successes. What happens along the way that causes such failure?

It's been more than 7 years since we started YC. In that time, we've funded 467 startups so I've seen a lot of patterns. There's a talk I always want to give at the beginning of each batch, warning everyone about things that I know are probably going to happen to them. I finally wrote down all my thoughts and I'm going to share them with you now.

We all know that a lot of smart and talented people start startups. You see huge numbers of startups getting started, and yet there are actually only a handful of startups that are big successes. What happens along the way that causes such failure?

It's like there's a tunnel full of monsters that kill them along the way. I'm going to tell you what these monsters are so you know to avoid them.

Determination

In general, your best weapon against these monsters is determination. Even though we usually use one word for it, determination is really two separate things: resilience and drive. Resilience keeps you from being pushed backwards. Drive moves you forwards.

One reason you need resilience in a startup is that you are going to get rejected a lot. Even the most famous startups had surprising amounts of rejection early on.

Everyone you encounter will have doubts about what you're doing—investors, potential employees, reporters, your family and friends. What you don't realize until you start a startup is how much external validation you've gotten for the conservative choices you've made in the past. You go to college and everyone says, "Great!" Then you graduate get a job at Google and everyone says, "Great!"

What do you think people say when you quit your job to start a company to rent out airbeds?

Determination

In general, your best weapon against these monsters is determination. Even though we usually use one word for it, determination is really two separate things: resilience and drive. Resilience keeps you from being pushed backwards. Drive moves you forwards.

One reason you need resilience in a startup is that you are going to get rejected a lot. Even the most famous startups had surprising amounts of rejection early on.

Everyone you encounter will have doubts about what you're doing—investors, potential employees, reporters, your family and friends. What you don't realize until you start a startup is how much external validation you've gotten for the conservative choices you've made in the past. You go to college and everyone says, "Great!" Then you graduate get a job at Google and everyone says, "Great!"

What do you think people say when you quit your job to start a company to rent out airbeds?

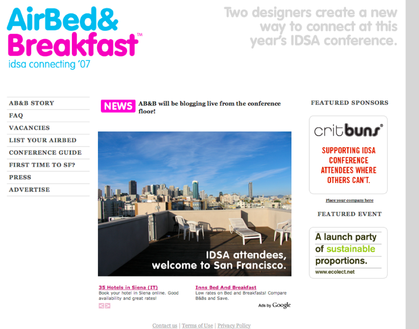

Check out Airbnb's website when they first launched in 2007. Here's how they describe what they do: Two designers create a way to connect at the IDSA conference. Have you even heard of the IDSA conference? Also, it was only for airbeds!

This is not the sort of thing you get a lot of external validation for. Almost everyone is more impressed with you if you get a job at Google than if you make a website for people to rent out airbeds for conferences.

Yet this is one of the most successful startups. Even if you are Airbnb, you are going to start out looking like an ugly duckling to most people.

When Airbnb did YC back in early 2009, they had already endured tons of rejection. (Check out Brian Chesky's talk from Startup School in 2010. It's one of the most inspirational stories out there.) By the time they came to us, they had maxed out their credit cards. They were eating leftover Capn McCain cereal. They were at the end of their rope.

Everyone thought their idea was crazy at the time—even I did actually—but they knew they were on to something. During YC, they made some key changes to their site, talked to users, set their goals, and measured everything. And the graphs started going up.

Remember that new ideas usually seem crazy at first. But if you have a good idea and you execute well, eventually everyone will see it.

We funded Eric Migicovsky about two years ago when he was working on Inpulse, the predecessor to the Pebble watch. Eric was a single founder and these watches have a quality that terrifies investors—they're hardware.

Poor Eric had a really hard time getting funding. No one wanted to fund a hardware company. He met with lots of investors who'd say things like, "I love the idea. But I can't fund a hardware company." Some claimed they just didn't fund hardware as a rule, others said that there were too many capital expenses up front. They all said no when he showed them the concept.

He'd been building the Pebble based on a lot of user feedback from the Inpulse, and he felt strongly that people wanted this product. So I remember he talked to Paul and they agreed he should give up on investors and put it on Kickstarter. His original goal was to raise $100,000 to make 1,000 watches. Instead of $100,000 Pebble raised $10.2mm in 30 days—the largest amount of money ever raised on Kickstarter. Now they are making 85,000 Pebbles.

Even Y Combinator got rejected when we first started back in Cambridge, MA in the summer of '05. Now there are lots of organizations doing what we do, but trust me, when we first started, people thought we were crazy. Or just stupid. Even our own lawyers tried to talk us out of it.

But 8 teams of founders took a chance on us and moved to Cambridge and got their $12,000 per team. I think they'd tell you that they had a great experience. We, too, knew we had hit on something interesting. So we focused on making something that a few people loved and we just expanded slowly from there.

But it was a slow process. When we came out to Silicon Valley in the winter of '06 we hardly knew anyone, so we decided to try to meet more investors to convince them to come to Demo Day . I got an introduction to the number one angel in the Valley, Ron Conway. Let me show you how he tried to brush us off.

This is not the sort of thing you get a lot of external validation for. Almost everyone is more impressed with you if you get a job at Google than if you make a website for people to rent out airbeds for conferences.

Yet this is one of the most successful startups. Even if you are Airbnb, you are going to start out looking like an ugly duckling to most people.

When Airbnb did YC back in early 2009, they had already endured tons of rejection. (Check out Brian Chesky's talk from Startup School in 2010. It's one of the most inspirational stories out there.) By the time they came to us, they had maxed out their credit cards. They were eating leftover Capn McCain cereal. They were at the end of their rope.

Everyone thought their idea was crazy at the time—even I did actually—but they knew they were on to something. During YC, they made some key changes to their site, talked to users, set their goals, and measured everything. And the graphs started going up.

Remember that new ideas usually seem crazy at first. But if you have a good idea and you execute well, eventually everyone will see it.

We funded Eric Migicovsky about two years ago when he was working on Inpulse, the predecessor to the Pebble watch. Eric was a single founder and these watches have a quality that terrifies investors—they're hardware.

Poor Eric had a really hard time getting funding. No one wanted to fund a hardware company. He met with lots of investors who'd say things like, "I love the idea. But I can't fund a hardware company." Some claimed they just didn't fund hardware as a rule, others said that there were too many capital expenses up front. They all said no when he showed them the concept.

He'd been building the Pebble based on a lot of user feedback from the Inpulse, and he felt strongly that people wanted this product. So I remember he talked to Paul and they agreed he should give up on investors and put it on Kickstarter. His original goal was to raise $100,000 to make 1,000 watches. Instead of $100,000 Pebble raised $10.2mm in 30 days—the largest amount of money ever raised on Kickstarter. Now they are making 85,000 Pebbles.

Even Y Combinator got rejected when we first started back in Cambridge, MA in the summer of '05. Now there are lots of organizations doing what we do, but trust me, when we first started, people thought we were crazy. Or just stupid. Even our own lawyers tried to talk us out of it.

But 8 teams of founders took a chance on us and moved to Cambridge and got their $12,000 per team. I think they'd tell you that they had a great experience. We, too, knew we had hit on something interesting. So we focused on making something that a few people loved and we just expanded slowly from there.

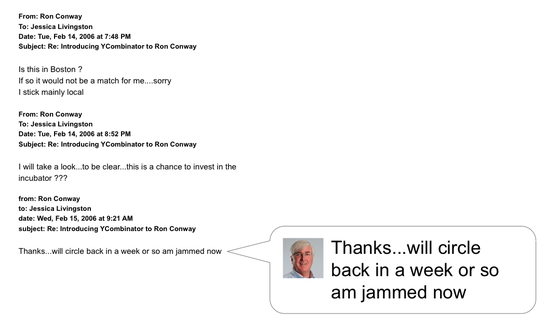

But it was a slow process. When we came out to Silicon Valley in the winter of '06 we hardly knew anyone, so we decided to try to meet more investors to convince them to come to Demo Day . I got an introduction to the number one angel in the Valley, Ron Conway. Let me show you how he tried to brush us off.

He said, "Is this in Boston? I stick mainly local." I replied, "No, we're in Mountain View and we'd love for you to come to Demo Day." He said, "Is this a chance to invest in the incubator?" I replied, "No, we don't want you to invest in us. It's a chance to invest in the individual startups." Then he told us he'd circle back, since he was jammed. We got the "am jammed now" from Ronco—it was so embarrassing.

It all worked out in the end though. He did wind up coming to Demo Day and he was impressed with what he saw. A year later, Ron came and spoke to the winter '07 batch of founders.

Variety of Problems

Remember, there were 2 components to determination: resilience and drive. We've talked about why you need resilience: because everyone will be down on you. You need drive to overcome the sheer variety of problems you will face in a startup.

Some of them are painfully specific—like a lawsuit or a deal blowing up—and some are demoralizingly vague: no one is visiting your site and you don't know why.

There's no playbook you can consult when these problems come up. You have to improvise. Sometimes you have to do things that seem kind of abnormal.

It all worked out in the end though. He did wind up coming to Demo Day and he was impressed with what he saw. A year later, Ron came and spoke to the winter '07 batch of founders.

Variety of Problems

Remember, there were 2 components to determination: resilience and drive. We've talked about why you need resilience: because everyone will be down on you. You need drive to overcome the sheer variety of problems you will face in a startup.

Some of them are painfully specific—like a lawsuit or a deal blowing up—and some are demoralizingly vague: no one is visiting your site and you don't know why.

There's no playbook you can consult when these problems come up. You have to improvise. Sometimes you have to do things that seem kind of abnormal.

Rajat Suri was a grad student at MIT when he started E La Carte. (E La Carte lets restaurant customers order and pay through a tablet.) He was so committed that he got a job as a waiter to learn what restaurants were like.

The Collison brothers founded Stripe, which does payment processing online. When these guys got started, they were a pair of young programmers. They had no idea how to make deals with banks and credit card companies.

I asked Patrick, "How did you even convince these big companies to work with you?" One trick that worked was to start with a phone call. Then people would pay attention to their arguments without being distracted by their youth. By the time they met in person and the companies could tell how young they were, they were already impressed.

The Collison brothers founded Stripe, which does payment processing online. When these guys got started, they were a pair of young programmers. They had no idea how to make deals with banks and credit card companies.

I asked Patrick, "How did you even convince these big companies to work with you?" One trick that worked was to start with a phone call. Then people would pay attention to their arguments without being distracted by their youth. By the time they met in person and the companies could tell how young they were, they were already impressed.

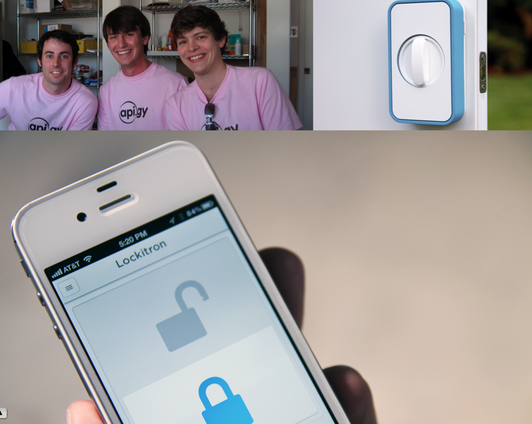

We funded the Lockitron guys back in the summer of '09—that's them at their YC interview. A year after YC, they were still figuring out their idea. They lived with the Wepay guys and one day the Wepays had a party for their investors. By that point the Lockitrons were working on a product to lock your door with an iPhone. They were able to impress one of the investors with their prototype, and he asked to have 40 installed in some startup offices he owned. The founders were psyched, but the commercial locks they needed to use cost $500 a pop. They didn't have $20,000 to fulfill an order that big. So they went around to the local locksmiths and scrapyards, buying broken locks for about $10 each. They fixed them themselves and were able to deliver on that order.

Fast forward a few years later: these guys were ready to launch the newest version of the Lockitron and decided go on Kickstarter. And guess what? A day after Lockitron submitted their campaign, Kickstarter changed their policy about hardware companies and rejected them. The Lockitron guys decided to build their own Kickstarter and they did it in less than a week. They wondered if anyone would even come. Not only did people come, but they've already sold close to $2 million dollars' worth of Lockitrons this way. And they didn't need to give a cut to Kickstarter.

Let me give you one last example of improvising. The Justin.tv founders were having a lot of scaling issues in the beginning. One weekend their whole video system went down. Kyle was in charge of it, but no one knew where Kyle was. And Kyle wasn't picking up his cell phone. This was live video so it was pretty critical that this get fixed immediately.

Michael Siebel called Kyle's friends and found out he was in Lake Tahoe and got the address of the house. So here's a problem for you, you know the address where someone is and he's not answering his phone. How do you get a message to him right away? Michael went on Yelp and looked for a pizza place near the house and called them up and said, "I want to have a pizza delivered. But never mind the pizza. Just send a delivery guy over and say these four words: The site is down." The pizza place was very confused by this, but they send the pizza guy without a pizza, Kyle answers the door, and the pizza guy says, "The site is down." Kyle was able to fix it, and the site was down for less than an hour total from beginning to end.

Cofounder Disputes

Another monster is cofounder disputes. People underestimate how critical founder relationships are to the success of a startup.

Unfortunately, I've seen more founder breakups than I care to count. And when it happens, it can crush a startup.

Be very careful when you decide to start a startup with someone. Do you know them well? Have you worked with them, gone to school with them? Don't slap yourself together with someone just because they are available and seem good enough. You'll probably regret it.

And if you start seeing red flags, do something about it. Don't think that it will go away. It's a red flag when you find yourself worrying whether your cofounder is trustworthy or whether he/she works hard enough or is competent.

When founders break up for whatever reason, it's a blow to the startup's productivity and morale. If there are three and one leaves, it's not so bad, but if there are two and one leaves, that's bad, because now you are a single founder and it's hard to do a startup as a single founder.

Investors

Investors tend to have a herd mentality. They like you if other investors like you.

So if no investor likes you until others do, what happens when you talk to the first ones? No one likes you! It's like the catch 22 of not being able to get a job because you don't have enough experience.

You are essentially starting off in a hole and you have to work your way out. You have to meet with lots investors and hear things like "I'd be interested once you have more traction" or "Who else is investing?"

If you work hard enough, you may be able to find a few who are excited enough about you and the idea that they aren't put off by the fact that you don't have any investors yet. Then when you have a few investors, you can start to make the herd mentality work for you instead of against you. Fundraising is slow and hard until it's fast and easy.

But working to convince those first few investors can be really demoralizing. It's a grind. (There are some really good investors who aren't like this, but the median investor is a herd animal.)

Investors will also drag their feet. Left to their own devices they'll just keep delaying. There's no downside for them to delay, whereas delay will kill you, because while you are fundraising your company will grind to a halt.

It blows my mind how many successful startups had a hard time fundraising at first. If you remember one piece of advice about investors, it's that you've got to create some type of competitive situation.

I'll give you what has always stuck in my mind as the most amazing example of this: one of the founders of one of our more successful startups had a longstanding relationship with a VC. When the founder started the company and did YC, this VC kept in touch through the 3 months, not really doing anything except keeping a benevolent eye on him. The VC attended demo day, but didn't invest. After a few months, the startup got a termsheet from a prestigious VC. When the first VC heard about this, he shifted into panic mode. He faxed the founder a termsheet from his firm with the valuation blank and said, "Fill in whatever valuation you want and we're in."

There are worse things investors can do to you than just delay. Sometimes they say yes and then change their mind. It's not a deal till the money is in the bank. We've seen some founders learn that they hard way.

I could tell you a lot of horror stories to frighten you, but just remember that fundraising is a bitch.

YC founders get to raise money under the best of circumstances and even for them it's a bitch.

Distractions

One of the reasons fundraising can be so damaging to your company is that it's a distraction.

We warn everyone early on at YC to be very careful about distractions. Nobody is stupid enough to get distracted by things that aren't work-related, like playing video games. The kind of distractions founders fall for are things that seem like a reasonable way to spend their time.

We tell people that during YC there are really only three things you should focus on: building things, talking to users, and exercising. Maybe this is a bit extreme, but the point is that early on in a startup all that matters is figuring out how to make something people want and doing it well. Don't spend all your time networking. Don't hire an army of interns. Just build stuff and talk to users.

(BTW, fundraising is a distraction, but it is necessary. So just try to spend as little time on it as possible.)

One thing that isn't necessary, and is a bad distraction, is talking to corporate development (or corp dev) people. These are the people at big companies who buy startups. You get a call from a corp dev person and they want to learn more about what you are doing and explore possible ways of working together. The founder thinks, "Oh boy, this important company wants to work with me. I should at least take a meeting."

I hate to sound harsh, but what these meetings really are for is for them to see if they want to do an HR acquisition.

HR Acquisitions

An HR acquisition means a company is essentially trying to hire you. (They are such a dangerous distraction that they get their own little monster!)

There's nothing wrong with HR acquisitions, if that's what you want to do. But most founders don't start startups just to go get a job a big company with what amounts to a nice hiring bonus.

Talking to corp dev early on isn't just a waste of time, it's uniquely demoralizing. I see this cycle happen over and over: the founders go to meet the corp dev people and think the meeting went great. They seemed so friendly and enthusiastic. The founders delude themselves into thinking that their startup is going to be the one that gets bought for $10 million after only 5 months. The founders start to think, "Yeah, we'd kind of like to get acquired," and then they start not to work on their startup as much and they lose momentum. Then they get the offer and it's essentially what they would have gotten if they walked in off the street and got a job. But by then they've gotten so accustomed to the idea of selling that they take it.

So going down the corp dev road seriously can deflate your ambitions. HR acquisitions are what you do when you are failing. Don't pull the cord on your inflatable life raft until your ship is actually sinking!

Making Something People Want is Hard

Now we come to the fiercest monster of all: the difficulty of making something people want. It's so hard that most startups aren't able to do it. You are trying to figure out something that's never been done before.

Not making something people want is the biggest cause of failure we see early on. (The second biggest is founder disputes.)

In order to make something people want, being brilliant and determined is not enough. You have to be able to talk to your users and adjust your idea accordingly. Ordinarily you have to change your idea quite a lot even if you start out with a reasonably good one.

Remember the first Airbnb website? Airbedandbreakfast was a rather narrower idea when they first launched. They started out as a site that let people rent out airbeds to travelers for conferences. Then they changed to renting out airbeds. Then they changed to renting out a room or a couch, but the host had to be there to make breakfast. Then finally they realized there was pent up demand to rent out entire places.

This evolution shows that you may begin with a general vision of what your startup is doing but you often have to try several different approaches to get it right.

Sometimes you have to totally change your idea. OrderAhead (which lets you order takeout on your cell phone) was the founders' 6th idea.

Even if you don't need to change the overall idea much, you still tend to have to do a lot of refinement. One of the best examples of this is Dropbox. Drew and Arash were working on something that was obviously necessary, but the reason it was hard to predict early on whether they'd succeed is that there were lots of people doing this. The way to win in this world was to execute well. It didn't just happen overnight; they had to get 1001 details right. There were a lot of unglamorous schleps between this photo:

Fast forward a few years later: these guys were ready to launch the newest version of the Lockitron and decided go on Kickstarter. And guess what? A day after Lockitron submitted their campaign, Kickstarter changed their policy about hardware companies and rejected them. The Lockitron guys decided to build their own Kickstarter and they did it in less than a week. They wondered if anyone would even come. Not only did people come, but they've already sold close to $2 million dollars' worth of Lockitrons this way. And they didn't need to give a cut to Kickstarter.

Let me give you one last example of improvising. The Justin.tv founders were having a lot of scaling issues in the beginning. One weekend their whole video system went down. Kyle was in charge of it, but no one knew where Kyle was. And Kyle wasn't picking up his cell phone. This was live video so it was pretty critical that this get fixed immediately.

Michael Siebel called Kyle's friends and found out he was in Lake Tahoe and got the address of the house. So here's a problem for you, you know the address where someone is and he's not answering his phone. How do you get a message to him right away? Michael went on Yelp and looked for a pizza place near the house and called them up and said, "I want to have a pizza delivered. But never mind the pizza. Just send a delivery guy over and say these four words: The site is down." The pizza place was very confused by this, but they send the pizza guy without a pizza, Kyle answers the door, and the pizza guy says, "The site is down." Kyle was able to fix it, and the site was down for less than an hour total from beginning to end.

Cofounder Disputes

Another monster is cofounder disputes. People underestimate how critical founder relationships are to the success of a startup.

Unfortunately, I've seen more founder breakups than I care to count. And when it happens, it can crush a startup.

Be very careful when you decide to start a startup with someone. Do you know them well? Have you worked with them, gone to school with them? Don't slap yourself together with someone just because they are available and seem good enough. You'll probably regret it.

And if you start seeing red flags, do something about it. Don't think that it will go away. It's a red flag when you find yourself worrying whether your cofounder is trustworthy or whether he/she works hard enough or is competent.

When founders break up for whatever reason, it's a blow to the startup's productivity and morale. If there are three and one leaves, it's not so bad, but if there are two and one leaves, that's bad, because now you are a single founder and it's hard to do a startup as a single founder.

Investors

Investors tend to have a herd mentality. They like you if other investors like you.

So if no investor likes you until others do, what happens when you talk to the first ones? No one likes you! It's like the catch 22 of not being able to get a job because you don't have enough experience.

You are essentially starting off in a hole and you have to work your way out. You have to meet with lots investors and hear things like "I'd be interested once you have more traction" or "Who else is investing?"

If you work hard enough, you may be able to find a few who are excited enough about you and the idea that they aren't put off by the fact that you don't have any investors yet. Then when you have a few investors, you can start to make the herd mentality work for you instead of against you. Fundraising is slow and hard until it's fast and easy.

But working to convince those first few investors can be really demoralizing. It's a grind. (There are some really good investors who aren't like this, but the median investor is a herd animal.)

Investors will also drag their feet. Left to their own devices they'll just keep delaying. There's no downside for them to delay, whereas delay will kill you, because while you are fundraising your company will grind to a halt.

It blows my mind how many successful startups had a hard time fundraising at first. If you remember one piece of advice about investors, it's that you've got to create some type of competitive situation.

I'll give you what has always stuck in my mind as the most amazing example of this: one of the founders of one of our more successful startups had a longstanding relationship with a VC. When the founder started the company and did YC, this VC kept in touch through the 3 months, not really doing anything except keeping a benevolent eye on him. The VC attended demo day, but didn't invest. After a few months, the startup got a termsheet from a prestigious VC. When the first VC heard about this, he shifted into panic mode. He faxed the founder a termsheet from his firm with the valuation blank and said, "Fill in whatever valuation you want and we're in."

There are worse things investors can do to you than just delay. Sometimes they say yes and then change their mind. It's not a deal till the money is in the bank. We've seen some founders learn that they hard way.

I could tell you a lot of horror stories to frighten you, but just remember that fundraising is a bitch.

YC founders get to raise money under the best of circumstances and even for them it's a bitch.

Distractions

One of the reasons fundraising can be so damaging to your company is that it's a distraction.

We warn everyone early on at YC to be very careful about distractions. Nobody is stupid enough to get distracted by things that aren't work-related, like playing video games. The kind of distractions founders fall for are things that seem like a reasonable way to spend their time.

We tell people that during YC there are really only three things you should focus on: building things, talking to users, and exercising. Maybe this is a bit extreme, but the point is that early on in a startup all that matters is figuring out how to make something people want and doing it well. Don't spend all your time networking. Don't hire an army of interns. Just build stuff and talk to users.

(BTW, fundraising is a distraction, but it is necessary. So just try to spend as little time on it as possible.)

One thing that isn't necessary, and is a bad distraction, is talking to corporate development (or corp dev) people. These are the people at big companies who buy startups. You get a call from a corp dev person and they want to learn more about what you are doing and explore possible ways of working together. The founder thinks, "Oh boy, this important company wants to work with me. I should at least take a meeting."

I hate to sound harsh, but what these meetings really are for is for them to see if they want to do an HR acquisition.

HR Acquisitions

An HR acquisition means a company is essentially trying to hire you. (They are such a dangerous distraction that they get their own little monster!)

There's nothing wrong with HR acquisitions, if that's what you want to do. But most founders don't start startups just to go get a job a big company with what amounts to a nice hiring bonus.

Talking to corp dev early on isn't just a waste of time, it's uniquely demoralizing. I see this cycle happen over and over: the founders go to meet the corp dev people and think the meeting went great. They seemed so friendly and enthusiastic. The founders delude themselves into thinking that their startup is going to be the one that gets bought for $10 million after only 5 months. The founders start to think, "Yeah, we'd kind of like to get acquired," and then they start not to work on their startup as much and they lose momentum. Then they get the offer and it's essentially what they would have gotten if they walked in off the street and got a job. But by then they've gotten so accustomed to the idea of selling that they take it.

So going down the corp dev road seriously can deflate your ambitions. HR acquisitions are what you do when you are failing. Don't pull the cord on your inflatable life raft until your ship is actually sinking!

Making Something People Want is Hard

Now we come to the fiercest monster of all: the difficulty of making something people want. It's so hard that most startups aren't able to do it. You are trying to figure out something that's never been done before.

Not making something people want is the biggest cause of failure we see early on. (The second biggest is founder disputes.)

In order to make something people want, being brilliant and determined is not enough. You have to be able to talk to your users and adjust your idea accordingly. Ordinarily you have to change your idea quite a lot even if you start out with a reasonably good one.

Remember the first Airbnb website? Airbedandbreakfast was a rather narrower idea when they first launched. They started out as a site that let people rent out airbeds to travelers for conferences. Then they changed to renting out airbeds. Then they changed to renting out a room or a couch, but the host had to be there to make breakfast. Then finally they realized there was pent up demand to rent out entire places.

This evolution shows that you may begin with a general vision of what your startup is doing but you often have to try several different approaches to get it right.

Sometimes you have to totally change your idea. OrderAhead (which lets you order takeout on your cell phone) was the founders' 6th idea.

Even if you don't need to change the overall idea much, you still tend to have to do a lot of refinement. One of the best examples of this is Dropbox. Drew and Arash were working on something that was obviously necessary, but the reason it was hard to predict early on whether they'd succeed is that there were lots of people doing this. The way to win in this world was to execute well. It didn't just happen overnight; they had to get 1001 details right. There were a lot of unglamorous schleps between this photo:

and this one:

Rollercoaster

Between starting the company and being on the cover of Forbes, you're going to have some dramatic ups and downs. In a startup, you don't have the damping that you'd have as part of a larger organization.

Circumstances fling you about. The process is often described as a roller coaster, because you are up one minute and down the next.

Lots of rollercoaster stories involve fundraising. One of the most extreme ones I know happened to some people we funded at their previous startup. It was based in Texas and they got a termsheet from a top tier VC in Silicon Valley. One of the conditions was that they base the company in the Bay Area. So the founders sold their homes and moved their families into corporate housing in Texas until they found new places in the Valley.

The documents were already signed and the money was scheduled to be wired on a friday. They were going to start working on monday out of the VC's office. So friday came and for some reason the money

didn't get wired. They called VC to ask if they should come out. The VC said, "Yes. Of course!" They got in their minivan and drove from Texas to Silicon Valley, stopping in Vegas to celebrate (this is the up part of the roller coaster).

On monday, they set up their stuff in conference room of the VC fund—all 6 of the team working there. By that wednesday, the funds still hadn't been wired. They had board meeting planned for that day and invited the VC.

In this meeting, the CEO talked about how signup numbers had gone down temporarily because they changed the way they measured them.

You know how this story will turn out...the VC had actually gotten buyer's remorse and he used this as an excuse to break the deal. Remember, they had signed all the documents, sold their houses, moved to Silicon Valley and were just waiting to get the $7 million wired to them. Instead the VC bails. He kicks them out of the conference room. The founders had to call their wives back in Texas and go back with their tails between legs. They had to lay everyone off. Can you imagine? Just a few days before they were celebrating in Vegas and now they have nothing.

(Incidentally, to get a story this extreme, we had to use an example of a startup we didn't fund. A VC probably wouldn't do this to a startup we had funded.)

Now let me tell you about the other half of the roller coaster:

We funded the Codecademy team in summer of 2011. Their original idea didn't work and they kept exploring new ones. It wasn't until late July that they started working on the idea of teaching people to code online. They launched just 3 days before Demo Day. In those 3 days, they got over 200,000 users.

They only launched so they could get up on Demo Day and say that they were a launched company. They never expected that in just 3 days they could go from a startup with an unlaunched idea to a startup that could get up on stage and announce they had 200,000 users (which is just about the most exciting thing you could say to investors).

The theme here is how extreme things can be. Just remember that no extreme ever lasts. Don't let yourself get immobilized by sadness when things go wrong. Just keep putting one foot in front of the other and know it will get better. But don't get complacent when things are going well. In reality things are never as bad or as

good as they seem.

What makes the rollercoaster even worse is that while you are on it, there's an audience watching everything you do. You'll have trolls and reporters saying outrageous things about you online. So be ready for this and have a thick skin.

Hard, But Not Impossible

Everyone knows that startups are hard. Yet when we watch people do it they are always surprised.

The reason they are surprised is that they don't realize how bad these specific problems can be. I've seen some very smart and talented people get so demoralized that they just gave up.

Startups are not for the faint of heart. I realize that this is not new news, but I wanted you to at least understand how they're hard early on so that when you run into these specific monsters, you'll know what to do.

Between starting the company and being on the cover of Forbes, you're going to have some dramatic ups and downs. In a startup, you don't have the damping that you'd have as part of a larger organization.

Circumstances fling you about. The process is often described as a roller coaster, because you are up one minute and down the next.

Lots of rollercoaster stories involve fundraising. One of the most extreme ones I know happened to some people we funded at their previous startup. It was based in Texas and they got a termsheet from a top tier VC in Silicon Valley. One of the conditions was that they base the company in the Bay Area. So the founders sold their homes and moved their families into corporate housing in Texas until they found new places in the Valley.

The documents were already signed and the money was scheduled to be wired on a friday. They were going to start working on monday out of the VC's office. So friday came and for some reason the money

didn't get wired. They called VC to ask if they should come out. The VC said, "Yes. Of course!" They got in their minivan and drove from Texas to Silicon Valley, stopping in Vegas to celebrate (this is the up part of the roller coaster).

On monday, they set up their stuff in conference room of the VC fund—all 6 of the team working there. By that wednesday, the funds still hadn't been wired. They had board meeting planned for that day and invited the VC.

In this meeting, the CEO talked about how signup numbers had gone down temporarily because they changed the way they measured them.

You know how this story will turn out...the VC had actually gotten buyer's remorse and he used this as an excuse to break the deal. Remember, they had signed all the documents, sold their houses, moved to Silicon Valley and were just waiting to get the $7 million wired to them. Instead the VC bails. He kicks them out of the conference room. The founders had to call their wives back in Texas and go back with their tails between legs. They had to lay everyone off. Can you imagine? Just a few days before they were celebrating in Vegas and now they have nothing.

(Incidentally, to get a story this extreme, we had to use an example of a startup we didn't fund. A VC probably wouldn't do this to a startup we had funded.)

Now let me tell you about the other half of the roller coaster:

We funded the Codecademy team in summer of 2011. Their original idea didn't work and they kept exploring new ones. It wasn't until late July that they started working on the idea of teaching people to code online. They launched just 3 days before Demo Day. In those 3 days, they got over 200,000 users.

They only launched so they could get up on Demo Day and say that they were a launched company. They never expected that in just 3 days they could go from a startup with an unlaunched idea to a startup that could get up on stage and announce they had 200,000 users (which is just about the most exciting thing you could say to investors).

The theme here is how extreme things can be. Just remember that no extreme ever lasts. Don't let yourself get immobilized by sadness when things go wrong. Just keep putting one foot in front of the other and know it will get better. But don't get complacent when things are going well. In reality things are never as bad or as

good as they seem.

What makes the rollercoaster even worse is that while you are on it, there's an audience watching everything you do. You'll have trolls and reporters saying outrageous things about you online. So be ready for this and have a thick skin.

Hard, But Not Impossible

Everyone knows that startups are hard. Yet when we watch people do it they are always surprised.

The reason they are surprised is that they don't realize how bad these specific problems can be. I've seen some very smart and talented people get so demoralized that they just gave up.

Startups are not for the faint of heart. I realize that this is not new news, but I wanted you to at least understand how they're hard early on so that when you run into these specific monsters, you'll know what to do.